Flexible Security: Decoding PM-SYM Exit and Withdrawal Rules 2026

- Mar 27

- 3 min read

As of Friday, March 27, 2026, the pm-sym (Pradhan Mantri Shram Yogi Maandhan) has successfully adapted to the "erratic nature of employment" in the unorganized sector. The government understands that a worker might face a sudden need for cash, a change in job status, or an unfortunate medical emergency.

Unlike many rigid pension plans, the shram yogi maandhan offers a "Voluntary Exit" module that was significantly upgraded in late 2025. This ensures that your hard-earned money is never truly "locked away" forever. Whether you've contributed for 2 years or 12, here are the official 2026 rules for getting your money back.

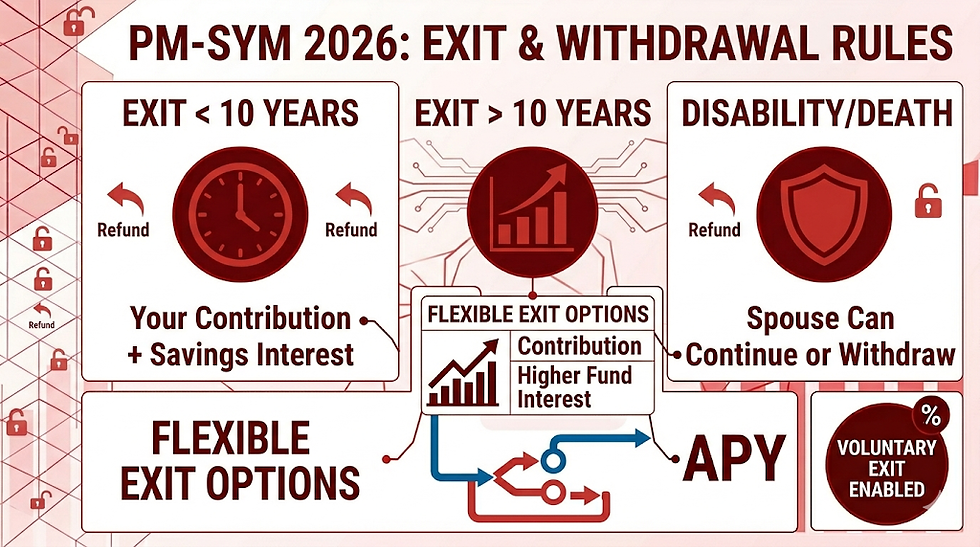

The Withdrawal Matrix: 2026 Edition

The amount you receive back depends entirely on how long you have been a regular subscriber to the pm-sym pension.

Scenario | Refund/Benefit Policy (2026) | Interest Rate Applied |

Exit within <10 Years | Only your share is returned. | Savings Bank Interest Rate. |

Exit after >10 Years | Your share is returned. | Higher of: Fund Interest or Savings Bank Interest. |

Move to Organized Sector | Account stays active or you can exit. | Savings Bank Interest Rate. |

Death before age 60 | Spouse can continue or withdraw. | Higher of: Fund Interest or Savings Bank Interest. |

Disability before age 60 | Spouse can continue or withdraw. | Higher of: Fund Interest or Savings Bank Interest. |

1. Premature Exit: Leaving Before 60

If you choose to leave the pm-sym voluntarily before reaching the retirement age:

Short-Term Exit (<10 years): If you exit within a decade of joining, the government keeps its matching share. You receive only the money you deposited, plus the standard savings bank interest (currently around 3-4%).

Long-Term Exit (>10 years): If you have been a loyal subscriber for over 10 years but haven't reached age 60, the government rewards you with better interest. You receive your share plus the actual interest earned by the LIC pension fund (which is usually higher than a savings bank).

2. What Happens in Case of Death or Disability?

The pm-sym pension is designed to protect the family unit, not just the individual.

Death before 60: If the subscriber passes away, the spouse has two choices. They can either continue the scheme by paying the same monthly installments until the subscriber would have turned 60, or they can exit and withdraw the full accumulated amount (subscriber's share + interest).

Permanent Disability: If a worker becomes permanently disabled and cannot work or pay installments, the spouse can take over. If the spouse also cannot continue, the account can be closed, and all subscriber contributions with interest are returned.

3. Moving to a Formal Job (EPFO/ESIC)

As of March 2026, there is a new "Migration Rule."

If you get a job that offers EPFO or ESIC, your pm-sym government contribution (50%) will stop because you are now an "Organized Worker."

You can either choose to pay the full 100% contribution yourself to keep the pension active or exit the scheme based on the "10-year rule" mentioned above.

4. FAQs: Getting Your Money Back

Q1. How do I apply for a refund?

Ans: You can initiate a "Voluntary Exit" through the maandhan.in portal using your login, or visit a CSC center. The money is credited directly to your linked bank account via DBT (Direct Benefit Transfer).

Q2. Does the government return its 50% share to me?

Ans: No. In almost all exit scenarios before age 60, the government’s matching contribution remains in the pension fund. You only receive the portion you paid from your own pocket.

Q3. What is the "Revival Module" for dormant accounts?

Ans: If you stopped paying but want to restart instead of exiting, the 2026 update allows you to revive a dormant account for up to 3 years by paying the arrears plus a small penalty.

Q4. What happens after the death of both the subscriber and spouse?

Ans: Unlike APY, in the pm-sym scheme, once both the subscriber and spouse have passed away, the entire remaining corpus is credited back to the Government Pension Fund. It is not returned to the children or nominees.

Conclusion

The pm-sym exit and withdrawal rules 2026 are built to be a "fair-weather friend." While the goal is to keep you invested until age 60 for the maximum ₹3,000 benefit, the scheme acknowledges that life happens. Knowing that you can get your contributions back with interest provides the peace of mind needed to start your pension journey today.

Comments