SpaceX $2 Trillion Valuation Explained: Is It Justified or Overhyped?

- 1 day ago

- 5 min read

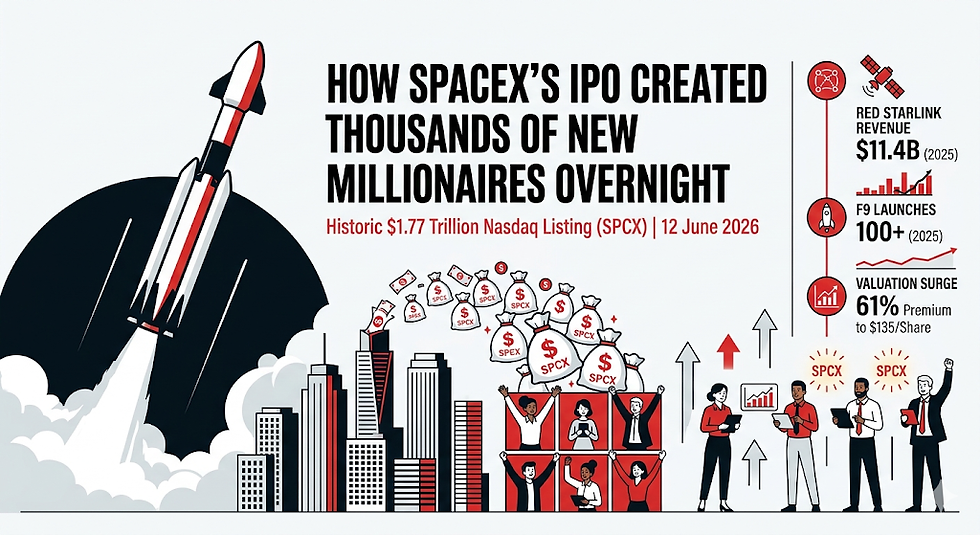

The financial world has officially entered a new epoch. In a historic Wall Street debut on Friday, June 12, 2026, SpaceX (NASDAQ: SPCX) executed the largest initial public offering (IPO) in human history. By raising a staggering $75 billion through the sale of over 555 million shares priced initially at $135, the company shattered the previous record set by Saudi Aramco in 2019.

But the real frenzy started when the opening bell rang. Driven by massive retail and institutional demand, the stock instantly surged over 20%, opening at $150 and quickly soaring past $166. This trading momentum officially pushed the company's market cap beyond an astronomical milestone. Today, we look at the reality behind the SpaceX $2 Trillion Valuation to see if this breathtaking number is backed by hard fundamentals or fueled by pure speculative hype.

Beyond making Elon Musk the world’s first official trillionaire, this listing has forced analysts to re-evaluate how we value a business that spans across global telecommunications, heavy defense contracts, deep-space exploration, and cutting-edge artificial intelligence.

The Raw Data: SpaceX’s Financials at a Glance

To understand if the valuation makes sense, we have to look directly at the S-1 filing and the latest 2026 financial data. Unlike mature tech giants that boast massive net profits, SpaceX operates heavily as a high-capex growth engine.

Here is a breakdown of the vital financial metrics guiding the market right now:

Financial Metric | 2025 / Q1 2026 Performance Data |

IPO Share Price | $135.00 |

Current Post-Debut Trading Price | $162.00 – $172.00+ |

Total Funds Raised via IPO | $75 Billion |

Full-Year 2025 Revenue | $18.7 Billion (Up 33% YoY from $14.1B in 2024) |

Adjusted EBITDA (2025) | $6.6 Billion |

Q1 2026 Net Loss | $4.28 Billion (Following a $4.94 Billion loss in 2025) |

Accumulated Deficit | $41.3 Billion |

Starlink Revenue Contribution | $11.4 Billion in 2025 (61% of total revenue) |

Quarterly AI Segment Losses | $2.5 Billion per quarter |

Why Bulls Say the SpaceX $2 Trillion Valuation is Justified

To traditional value investors, a company trading at over 100 times its trailing revenue while posting billions in net losses looks like a classic bubble. However, those buying into the SpaceX $2 Trillion Valuation are not buying a traditional aerospace firm; they are buying a multi-pronged monopoly with three distinct, high-moat business segments.

1. Starlink: The Cash-Cow Global Telecom Monopoly

Starlink is no longer an experimental satellite constellation—it is a dominant global utility. In 2025, Starlink generated $11.4 billion, accounting for over 61% of SpaceX’s entire revenue stream. In the first quarter of 2026, Starlink brought in $4.69 billion.

Importantly, Starlink’s connectivity arm is currently the only profitable part of the entire company. With roughly 9,600 satellites currently in orbit and regulatory approval to scale up to 100,000, Starlink is capturing high-margin maritime, aviation, rural residential, and military communication markets worldwide. It acts as an unbreakable recurring revenue subscription model that funds the rest of Musk's interplanetary ambitions.

2. Complete Launch Dominance and the Starship Factor

The core space launch unit handles nearly the entirety of Western orbital payloads. Between NASA’s multi-billion dollar Artemis lunar contracts and the Pentagon’s national security launch reliance, SpaceX faces no viable commercial competition.

While the space unit registered a technical loss of $619 million recently due to aggressive development cycles, the massive $75 billion cash injection from the June 2026 IPO will directly accelerate the deployment of Starship. Starship is designed to be completely reusable, bringing the cost per kilogram to orbit down to unprecedented lows.

3. The Hidden AI Play

Perhaps the biggest catalyst for the post-IPO stock surge is SpaceX's aggressive expansion into artificial intelligence. Capital expenditures crossed $10.1 billion last quarter, with a massive $7.7 billion allocated strictly to AI infrastructure.

While the AI wing is burning roughly $2.5 billion per quarter, investors see this as a foundational step. By merging real-time global Starlink data arrays with autonomous space navigation, defense robotics, and satellite-based geospatial intelligence, SpaceX is building a highly defensible physical AI network that traditional software companies cannot replicate.

Why Bears Call It Overhyped: The Risk Factors

While enthusiasm on the Nasdaq floor is undeniable, severe structural risks warrant caution. Critics argue that the current valuation relies on flawless execution in highly unstable environments.

Breathtaking Capital Burn: SpaceX posted an accumulated deficit of $41.3 billion ahead of its IPO, alongside a net loss of $4.28 billion in Q1 2026 alone. The company is spending money faster than almost any corporate entity on Earth.

Massive AI Depreciation and Drag: The $2.5 billion quarterly loss from the AI division means that any delays in monetizing their AI infrastructure could severely weigh down Starlink's profitability.

Key-Man Risk and Governance: Elon Musk retains 42% of the equity but controls a commanding 85% of the voting power. With his attention divided across Tesla, xAI, X (formerly Twitter), and political commitments, public shareholders have virtually no say in governance.

Geopolitical Vulnerability: Because Starlink acts as a critical defense communications backbone for the U.S. and its allies, it is a primary target for geopolitical adversaries, introducing regulatory and kinetic risks that standard tech companies never face.

Is It Justified or Overhyped? The Verdict

When assessing the SpaceX $2 Trillion Valuation, the conclusion depends entirely on your investment horizon.

If you analyze SpaceX using backward-looking GAAP accounting metrics, the valuation looks heavily overhyped. The company is losing billions, its capital expenditures are doubling year-over-year, and it relies on non-stop infrastructure deployment just to maintain its current market share.

However, if you look at SpaceX as a foundational layer of the future global economy, the price tag becomes understandable. It holds a near-absolute monopoly on space launch, owns the world's most extensive satellite internet grid, and is sitting on a fresh $75 billion war chest to fund Starship and AI development. For institutional mega-funds, SpaceX represents an irreplaceable macro asset class.

Frequently Asked Questions (FAQs)

Is the SpaceX $2 Trillion Valuation justified given its massive net losses?

While the company reports steep GAAP net losses—including $4.28 billion in Q1 2026 alone—proponents argue the SpaceX $2 Trillion Valuation is justified by its $6.6 billion in adjusted 2025 EBITDA and Starlink's strong cash generation. Most of the losses stem from heavy capital expenditures into long-term infrastructure, such as Starship development and their new $7.7 billion quarterly AI investments, rather than weak core operations.

What is the stock ticker for SpaceX and where does it trade?

SpaceX trades publicly on the Nasdaq under the ticker symbol SPCX. Its historic IPO occurred on June 12, 2026.

How much of SpaceX's revenue comes from Starlink?

Starlink is the primary financial driver of the company. In 2025, Starlink brought in $11.4 billion, which represents roughly 61% of SpaceX’s total $18.7 billion revenue.

Did the SpaceX IPO make Elon Musk a trillionaire?

Yes. Following the blockbuster Nasdaq debut where SPCX shares surged past $160 from the $135 IPO price, Elon Musk’s 38% equity stake in the company pushed his total net worth well past the $1 trillion mark, making him the first official trillionaire in history.

Stay Ahead of the Market

The public listing of SpaceX marks a turning point for retail and institutional investors alike. As the space economy continues to expand rapidly, keeping up with institutional data, S-1 amendments, and market shifts is essential.

Track Public Markets: Monitor live price action, trading volumes, and index inclusion updates directly via the Nasdaq SPCX Investor Relations Portal.

Review Official Disclosures: Read through the comprehensive risk factors, segment margins, and capital breakdown in the SEC EDGAR SpaceX S-1 Filing Database.

Follow Space Economy Trends: Stay updated on commercial launch schedules, Starlink constellation expansions, and global aerospace policy via the SpaceX Official Media Center.

Comments