SpaceX IPO Price at $135: Was the Stock Undervalued?

- 1 day ago

- 9 min read

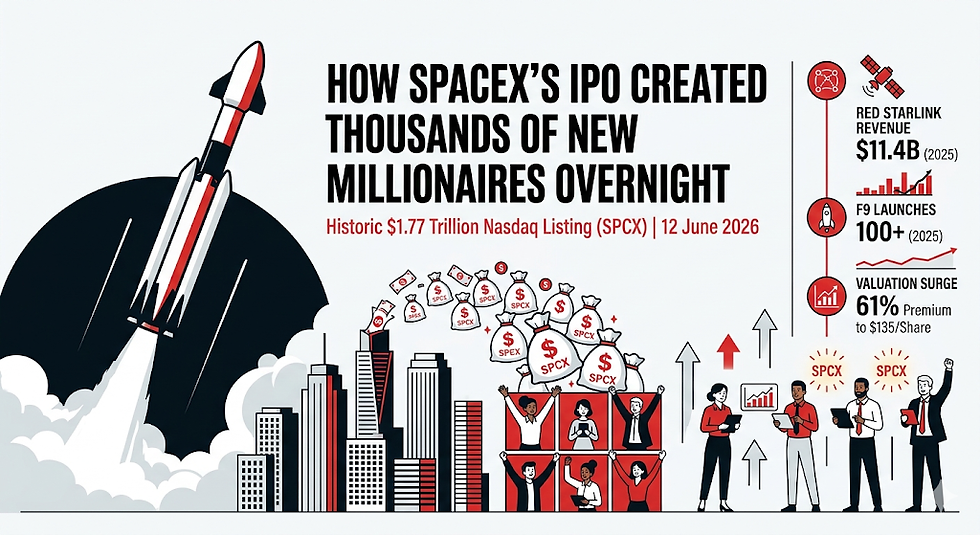

The global financial landscape just witnessed a historic milestone. On June 12, 2026, Elon Musk’s SpaceX officially made its long-awaited debut on the Nasdaq under the ticker symbol SPCX. Shattering every previous stock market record, the space powerhouse bypassed traditional pricing ranges to offer an ultimate take-it-or-leave-it SpaceX IPO price at $135 per share.

With 555.56 million Class A common shares issued, this blockbuster public debut raised a staggering $75 billion in net new capital, entirely bypassing any secondary Offer for Sale (OFS). This monumental debut cements SpaceX as the largest initial public offering in human history, easily eclipsing Saudi Aramco’s $29 billion capital raise in 2019. At the fixed issue price, SpaceX locked in an initial market capitalization of $1.77 trillion, making it the seventh-largest publicly traded corporation in the United States and the eighth-largest globally—shunting heavyweights like Saudi Aramco ($1.75T) and sister company Tesla ($1.49T) further down the leaderboard.

Yet, immediately upon the opening bell, Wall Street experienced absolute pandemonium. Retail demand surged to over $100 billion out of an aggregate order book that exceeded $250 billion—leaving the IPO roughly 3.5 to 4 times oversubscribed. When trading commenced at midday, the stock bypassed its initial threshold entirely, opening at $150 per share and surging past $170 within hours. This market mania officially catapulted Elon Musk into the history books as the world’s first-ever trillionaire, with a net worth peaking beyond $1.1 trillion.

But as the dust settles on day one, institutional analysts and retail investors alike are grappling with a multi-trillion-dollar question: Was the stock undervalued at $135, or is the public market blindly buying into hyper-extended cosmic euphoria? Let’s dive deep into the financials, the structural units, and the valuation models shaping SpaceX in 2026.

The Financial Anatomy of SpaceX: S-1 Prospectus Disclosures

To evaluate whether the SpaceX IPO price at $135 was truly a bargain, we must first analyze the hard financial data revealed in the company's SEC S-1 prospectus. For years, SpaceX operated inside a black box, offering rare glimpses of profitability via private secondary markets. The public filing has peeled back the layers, revealing a business that is simultaneously a hyper-growth cash cow and a massively expensive capital sinkhole.

Over the Last Twelve Months (LTM) leading into Q1 2026, SpaceX generated an impressive $18.67 billion in consolidated revenue. However, despite this massive top-line figure, the company is fundamentally unprofitable on a consolidated net basis. SpaceX disclosed a heavy net loss of $4.28 billion for Q1 2026, following a full-year net loss of $4.94 billion in 2025.

The underlying reality is that SpaceX is not a singular operating business; it is a conglomerate of three distinct segments, each operating on completely different financial planes.

1. The Connectivity Arm (Starlink)

Starlink is the undisputed crown jewel of SpaceX’s immediate financial viability. Operating as a massive satellite broadband mega-constellation providing high-speed internet to 164 countries, Starlink has scaled aggressively.

Quarterly Revenue: $4.69 billion (representing roughly 69% of SpaceX’s total quarterly revenue).

LTM Run Rate: Steady at $3.26 billion per quarter globally.

Profitability: It is the only profitable arm of the company, generating a solid $1.19 billion in operating profit per quarter.

Subscriber Base: Currently stands at 10.3 million active subscribers worldwide and continues to grow.

2. The Space Segment (Launch & Exploration)

This unit encompasses Falcon 9, Falcon Heavy, national security defense contracts, and the ongoing development of the massive Starship ecosystem in Starbase, Texas. Despite making more launch attempts than any individual nation-state in 2025 and effectively holding a monopoly over global commercial spaceflight, this segment operates at a deficit due to intense infrastructure spending.

Quarterly Performance: Logged an operating loss of $619 million in the latest quarter.

3. The Artificial Intelligence Arm (SpaceX-AI)

Formed via the rapid structural integration of Elon Musk's xAI startup into SpaceX earlier this year, this unit represents the company’s newest, riskiest, and most capital-intensive venture. SpaceX-AI pairs the global satellite footprint of Starlink with immense terrestrial and orbital computing power. This includes the proprietary "Colossus" data centers on Earth and multi-billion-dollar R&D roadmaps to build low-Earth-orbit AI data networks using laser cross-links.

Quarterly Performance: Logged a severe operating loss of $2.5 billion.

R&D Burn Rate: AI research and development spending skyrocketed by over 300%, topping $5.06 billion.

To put the financial weight of these segments into perspective, SpaceX’s total capital expenditures (CapEx) for the latest quarter reached $10.1 billion—more than doubling year-over-year. A staggering $7.7 billion of that single-quarter CapEx went directly into AI infrastructure and GPU procurement. Furthermore, the prospectus notes that SpaceX is carrying a mountain of $25.45 billion in contractual commitments, 95% of which must be settled over the 2026–2027 fiscal window.

SpaceX Full IPO Data Sheet (2026)

The following real table outlines the key metrics, structural parameters, and financial realities of the history-making SPCX public debut:

Parameter / Metric | Disclosed Value / Stat | Operational Notes & Strategic Implications |

Nasdaq Ticker | SPCX | Primary listing on Nasdaq Global Select; dual-listed on Nasdaq Texas. |

IPO Price | $135.00 Per Share | Fixed take-it-or-leave-it price; no standard indicative range provided. |

Market Capitalization | ~$1.77 Trillion | Valued at the $135 IPO price; soared past $2.2 Trillion post-market debut. |

Total Funds Raised | $75 Billion | Net new growth capital; 0% Offer for Sale (OFS) from existing insiders. |

Shares Outstanding Issued | 555,555,555 Shares | Class A common stock offered to the public; ~4% total float. |

Oversubscription Rate | 3.5x to 4.0x | Total institutional and retail aggregate demand topped $250 Billion. |

Retail Share Allocation | 20% to 30% | Unusually high allocation meant to democratize access for small investors. |

Lockup Period | 180 Days | Standard 6-month restriction preventing insiders and employees from selling. |

Voting Control | ~85% Control | Maintained completely by Elon Musk via super-voting Class B shares. |

LTM Revenue | $18.67 Billion | Trailing 12-month consolidated revenue up to Q1 2026. |

Q1 2026 Net Loss | $4.28 Billion | Driven by aggressive Starship scaling and multi-billion-dollar AI outlays. |

Starlink Subscriber Base | 10.3 Million | Active global subscriptions spanning across 164 countries. |

Contractual Commitments | $25.45 Billion | Fixed liabilities due immediately over the course of 2026 and 2027. |

Morningstar Fair Value | $780 Billion | Independent valuation pegging the equity at 48% below the IPO price. |

The Bull Case: Why $135 Was Undervalued

Long-term venture capitalists, growth-equity funds, and retail bulls argue that the SpaceX IPO price at $135 is a generational entry point, making the company fundamentally undervalued when viewing its multi-decade terminal value.

+-----------------------------------------------------------------+

| SPACEX VALUATION DRIVERS |

+-----------------------------------------------------------------+

| |

| [1. STARLINK MONOPOLY] ------> 10.3M Subs & 164 Countries |

| Generates $1.19B/Quarter Net |

| |

| [2. STARSHIP FREQUENCY] -----> Drastically Drops Launch Cost |

| Enables Orbital Mass Scale |

| |

| [3. SPACEX-AI SYNERGY] ------> Satellite Laser Network + |

| Colossus AI Data Centers |

| |

+-----------------------------------------------------------------+

1. Starlink is an Unstoppable Free-Cash-Flow Engine

At 10.3 million subscribers and counting, Starlink's consumer, maritime, aviation, and government defense segments (Starshield) are expanding exponentially. Because the foundational rocket infrastructure is manufactured in-house, Starlink enjoys a vertical integration advantage that legacy telecom consortia cannot replicate. Generating nearly $1.2 billion in net operating profit per quarter, Starlink is on a clear trajectory to become a standalone cash-flow monster capable of self-funding SpaceX’s deep-space initiatives.

2. The Starship Launch Monopoly

SpaceX has fundamentally rewritten the economics of orbital mechanics. The deployment of the fully reusable Starship launch system lowers the cost per kilogram to low Earth orbit (LEO) from thousands of dollars to double digits. This creates an insurmountable moat. Competitors like United Launch Alliance (ULA), Arianespace, and Blue Origin are lagging years behind in terms of launch cadence and reuse capability. SpaceX is effectively the sole gatekeeper to the burgeoning space economy.

3. The Unprecedented SpaceX-AI Integration Multiplier

By merging xAI into SpaceX, Elon Musk has created a unified data and computing giant. Starlink provides a resilient, low-latency global network capable of moving data anywhere on the planet without relying on terrestrial fiber networks. When paired with the "Colossus" supercomputing clusters and the Grok AI engine, SpaceX is uniquely positioned to build orbit-based AI data center networks. This enables sovereign cloud computing free from local geopolitical interference, opening up an entirely new market worth trillions.

4. Direct Injection of $75 Billion and Index Fast-Tracking

Because the $75 billion raised goes entirely to corporate cash reserves rather than an insider cash-out (OFS), SpaceX has a massive war chest to fund its CapEx without taking on high-interest debt. Furthermore, major index providers like the Nasdaq-100 recently overhauled their rules, dropping the historical 1-year "seasoning" requirement for mega-cap listings.

Effective May 2026, top-ranked companies exceeding $100 billion can be fast-tracked into key benchmarks in just 15 trading days. This structural shift forces trillions of passive index-tracking fund dollars to buy SPCX shares almost immediately, creating a structural floor under the stock price.

The Bear Case: Why $135 Was Highly Overvalued

Conversely, conservative institutional analysts look at the numbers and argue that the SpaceX IPO price at $135 represents peak market exuberance, disconnected from standard fundamental valuation principles.

1. Astronomical Valuation Multiples

At an initial market capitalization of $1.77 trillion against a trailing twelve-month revenue of $18.67 billion, SpaceX went public at an eye-watering price-to-sales (P/S) multiple of roughly 95x. For context, the broader tech-heavy Nasdaq index typically trades at a P/S multiple between 4x and 5x, while high-growth enterprise SaaS and AI hardware stocks hover around 20x to 35x. Paying nearly 100 times revenue for a capital-heavy business that loses billions each quarter requires flawless execution without any room for error.

2. Extreme Independent Valuation Discrepancies

Sobering quantitative assessments from traditional financial firms cast doubt on the multi-trillion-dollar price tag. Most notably, Morningstar’s independent Discounted Cash Flow (DCF) analysis pegged the fundamental fair value of SpaceX at $780 billion—a staggering 48% below the $135 IPO price.

Morningstar warned that retail investors blindly chasing the listing on day one face severe valuation risks. They noted that the integration of xAI introduces severe capital-expenditure strain and corporate governance conflicts of interest that could erode shareholder value.

3. The Enormous Cash Burn and AI R&D Pit

While bulls point to Starlink’s profitability, it is heavily offset by the sheer cash destruction across the other two arms. Losing over $4 billion in a single quarter is a massive burn rate, driven by a doubling of CapEx to $10.1 billion. The $5.06 billion spent on AI R&D and GPU clusters means SpaceX is now taking on massive tech-sector risks. If the global commercialization of generative AI experiences a cyclical slowdown or structural bottleneck, SpaceX will be stuck holding billions in depreciating hardware assets.

4. Massive Near-Term Contractual Liabilities

With $25.45 billion in contractual obligations due entirely through 2026 and 2027, a significant portion of the $75 billion raised will immediately flow toward clearing short-term debt and liabilities rather than pure long-term R&D. Any launch failure, orbital regulatory pushback, or geopolitical conflict affecting Starlink’s ground terminals could disrupt cash flow at a time when fixed liabilities are at an all-time high.

Technical vs. Fundamental Valuation: The Verdict

So, was the SpaceX IPO price at $135 undervalued? The answer depends entirely on your investment horizon and framework.

From a strict, traditional fundamental analysis perspective, the stock was undeniably overvalued at $135. A 95x revenue multiple for a company with a net quarterly loss of $4.28 billion and an independent fair-value estimate of $780 billion signals an expensive entry point. Investors buying at this level are paying for performance that likely won’t materialize on the bottom line until the 2030s.

However, from a strategic and technical market perspective, $135 proved to be an efficient entry price. The overwhelming 4x oversubscription rate and $250 billion in institutional demand proved that the market was more than willing to absorb the premium. Because the float is restricted to just 4% of total shares outstanding and Elon Musk retains absolute voting control (85%), scarcity dynamics drove the stock up on its first day. When you factor in the automated index-fund inclusion forcing passive managers to buy the stock, the initial $135 pricing left money on the table for public markets to capture.

Frequently Asked Questions (FAQs)

What was the official SpaceX IPO price at $135 per share implying for its total valuation?

The fixed SpaceX IPO price at $135 per share implied an initial company market capitalization of approximately $1.77 trillion. This historic valuation allowed SpaceX to enter the public markets as the seventh-largest publicly traded corporation in the United States and the eighth-largest in the world, positioning it just ahead of corporate giants like Saudi Aramco and Tesla.

Why did SpaceX choose a fixed $135 price instead of a traditional IPO pricing range?

SpaceX leadership utilized an aggressive, non-traditional "accept-it-or-leave-it" fixed pricing mechanism because they held maximum leverage over Wall Street. Knowing that institutional demand was wildly oversubscribed—ultimately reaching over $250 billion in total orders—the underwriters bypassed the traditional price-discovery range to lock in maximum capital directly at $135 per share.

Is SpaceX currently turning a profit?

No, on a consolidated corporate basis, SpaceX is not yet profitable. While its satellite internet division, Starlink, is highly profitable—bringing in $4.69 billion in revenue and generating a clean $1.19 billion in operating profit per quarter—the company logged an overall net loss of $4.28 billion for the first quarter of 2026. This net deficit is driven by massive capital expenditures into Starship development and over $5.06 billion in AI research and development.

How can international or retail investors buy SPCX stock?

Retail investors can purchase SPCX shares through standard brokerage platforms supporting Nasdaq-listed equities. For international retail investors, such as those in India, allocations can be accessed via compliant cross-border investment platforms, fractional US stock brokers, or dedicated international financial pathways established through institutional clearinghouses like GIFT City.

What are the main risk factors outlined in the SpaceX S-1 prospectus?

The primary risks include an incredibly high price-to-sales multiple (95x), a massive quarterly capital burn rate exceeding $10 billion, and $25.45 billion in fixed contractual commitments due across 2026-2027. Additionally, independent research firms like Morningstar consider the stock overvalued, warning that the heavy financial integration of Musk's AI arm presents severe capital allocation and governance risks.

Comments