SpaceX IPO and Starlink Growth: The Real Story Behind the Valuation

- 1 day ago

- 7 min read

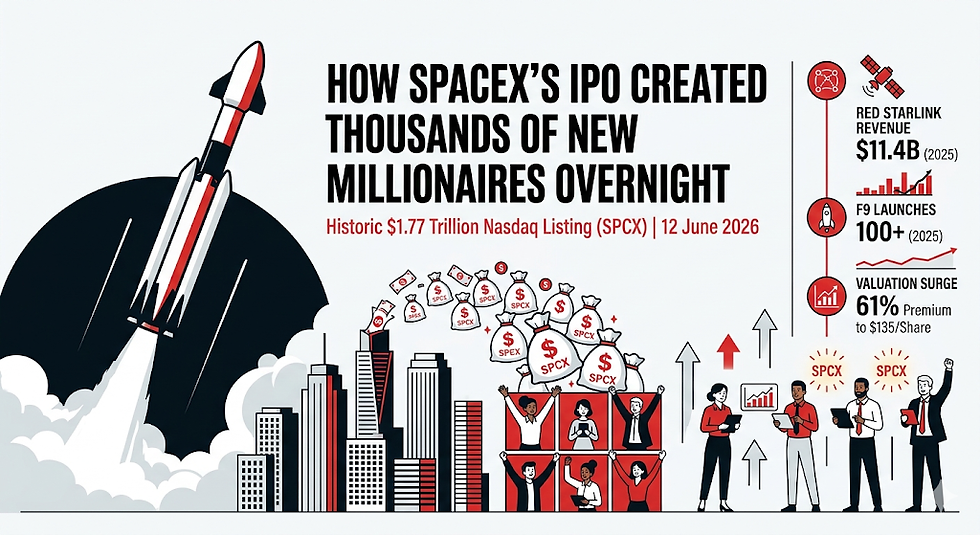

The financial world just witnessed history. On Friday, June 12, 2026, SpaceX officially debuted on the Nasdaq under the ticker SPCX, closing a monumental initial public offering that cemented its position as a global economic superpower.

With a final IPO price of $135 per share, the company raised a staggering $75 billion by floating 555.5 million shares. The market’s reaction was immediate and electric: the stock opened at $150—an 11% premium—and quickly pushed past a $2 trillion market cap in intraday trading. This massive surge officially crowned Elon Musk as the world’s first trillionaire.

Yet behind the breathless headlines lies a complex financial reality. The SpaceX IPO valuation of $1.77 trillion at listing makes it the largest initial public offering in history, eclipsing Saudi Aramco’s 2019 record. But is a company that posted a $4.28 billion net loss in the first quarter of 2026 alone truly worth more than Microsoft and Alphabet?

To understand the real story behind this eye-popping valuation, we have to look past the rockets and dissect the actual mechanics of its cash engine: Starlink.

The Financial S-1 Breakdown: What the Math Reveals

When SpaceX filed its highly confidential S-1 prospectus ahead of the IPO, Wall Street analysts finally got a look at the actual books of the notoriously secretive aerospace giant. The numbers reveal a dramatic, structural divide between massive top-line expansion and staggering capital expenditures.

+------------------------------------+-----------------------+

| Financial Metric | Fiscal Year 2025 / Q1 2026 Data |

+------------------------------------+-----------------------+

| Total 2025 Revenue | $18.7 Billion |

| Year-over-Year Revenue Growth | 33% (Up from $14.1B) |

| 2025 Adjusted EBITDA | $6.6 Billion |

| Full-Year 2025 Net Loss | $4.9 Billion |

| Q1 2026 Net Loss | $4.28 Billion |

| Total Accumulated Deficit | $41.3 Billion |

| Starlink 2025 Revenue | $11.4 Billion |

| Starlink 2025 Operating Income | $4.4 Billion |

+------------------------------------+-----------------------+

As the data shows, SpaceX generated $18.7 billion in total revenue for the full year 2025, a robust 33% increase over 2024. However, the company remains firmly in investment mode, burdened by a historic accumulated deficit of $41.3 billion.

The massive disconnect between its $6.6 billion in adjusted EBITDA and its multi-billion-dollar GAAP net losses is driven by three main factors:

Massive stock-based compensation.

High depreciation costs associated with aggressive satellite deployment.

Heavy capital expenditures required for its newly integrated artificial intelligence infrastructure.

Starlink Growth: The Cash Engine Powering the SpaceX IPO Valuation

If SpaceX were merely a launch provider, it would be valued as a defense contractor—perhaps worth $100 billion to $150 billion. The trillion-dollar premium built into the SpaceX IPO valuation is almost entirely a bet on Starlink revenue growth and its dominance in the global telecom landscape.

By the end of 2025, Starlink had definitively become SpaceX’s largest and only consistently profitable business segment. It generated $11.4 billion in revenue—accounting for roughly 61% of SpaceX’s entire top line—and brought in $4.4 billion in operating income.

The Rapid Ascent of Satellite Internet Subscribers

Starlink’s capacity to scale its user base has completely rewritten the playbook for satellite telecommunications. The service crossed 12 million satellite internet subscribers in June 2026, up sharply from 10.3 million at the end of Q1 2026, and more than double the 4.4 million subscribers it held in early 2025.

+----------------+------------------------+------------+

| Timeline | Approximate Subscribers| Estimated ARPU|

+----------------+------------------------+------------+

| December 2023 | 2.3 Million | $99 |

| December 2024 | 4.4 Million | $91 |

| December 2025 | 8.9 Million | $81 |

| March 2026 | 10.3 Million | $66 |

| June 2026 | 12.0 Million | Under $65 |

+----------------+------------------------+------------+

While the subscriber acquisition curve is steep, a underlying challenge has emerged: Average Revenue Per User (ARPU) is falling.

The ARPU Problem and the Push for Global Volume

As Starlink expands beyond affluent Western markets, it is moving aggressively into price-sensitive regions across Africa, Latin America, and Southeast Asia. To match local purchasing power, subscription fees in these regions are set significantly lower than US rates.

This strategy successfully drives sheer volume, but it puts a squeeze on margins. While total subscribers more than doubled year-over-year by early 2026, Starlink's quarterly operating income rose more modestly—from $1.03 billion to $1.19 billion.

Furthermore, Starlink is rapidly exhausting the "low-hanging fruit" of rural, completely unserved areas. To sustain its growth trajectory, it must now compete directly in suburban environments against established, terrestrial fiber, cable, and fixed wireless providers. These competitors can easily underbid satellite services on price-per-megabit and offer superior, weather-proof reliability.

The Three Pillars of the Trillion-Dollar Business Model

To justify its status as the eighth-largest publicly traded firm on earth, SpaceX pitched institutional investors on a highly diversified, multi-industry business model. In its S-1 filing, the company structured its operations into three distinct, hyper-scale reporting units:

1. Connectivity (Starlink & Starshield)

This core unit encompasses civilian broadband, maritime connections, aviation Wi-Fi, and Starshield—the highly classified military and government communication network. Starshield secure contracts with the Pentagon and NASA provide high-margin, recession-proof revenue that anchors the division's financial health.

2. Space Exploration (Falcon & Starship Development)

The launch division remains the undisputed king of orbital logistics, executing roughly 75% of all active maneuverable satellite launches globally. However, this segment operates under heavy financial strain.

The next-generation Starship development program absorbs billions of dollars in development costs. While Starship promises to reduce launch costs to unprecedented lows via total reusability, it remains in an intensive testing phase, requiring massive capital infusions to hit its lunar and Mars targets.

3. Artificial Intelligence and Compute Infrastructure (The xAI Merger)

The ultimate wild card in the SpaceX IPO valuation is its brand-new AI division. Following the blockbuster corporate merger between SpaceX and Elon Musk's xAI earlier this year, the company transformed overnight into an AI infrastructure heavyweight.

This unit brings together the Grok large language model, deep data integration with social platform X, and massive compute data centers. The AI segment is incredibly expensive, burning roughly $2.5 billion per quarter in AI-related infrastructure capex, which accounted for a staggering 76% of the group's total capital expenditures in Q1 2026.

To offset these eye-watering costs, SpaceX has begun renting out its massive compute clusters to third parties. A recently signed cloud-compute deal with Anthropic is set to generate $1.25 billion per month through May 2029, proving that the AI business can bring in serious commercial revenue.

Institutional Skepticism: Is SpaceX Overvalued?

The retail demand for the IPO was unprecedented, with the $75 billion offering becoming oversubscribed by nearly four times, raking in more than $250 billion in institutional bids. Yet, independent equity research firms are urging extreme caution.

"We believe the business has real strengths, particularly in Starlink, but with so many unknown and untested technologies underpinning much of the valuation price, particularly within the AI business, we think the valuation is extremely speculative." — Michael Field, Chief Equity Strategist at Morningstar

The Core Arguments Against the $1.77T+ Valuation:

Overstated Total Addressable Market (TAM): SpaceX marketing materials claim a massive $1.6 trillion TAM for Starlink, assuming it can compete directly with global telecom giants. Analysts point out that satellite broadband faces insurmountable physics and capacity constraints in dense urban environments, making it a niche solution for rural and mobile use rather than a total telecom disruptor.

The Valuation Disconnect: Morningstar’s quantitative valuation models peg the fair value of SpaceX at just $63 per share—a massive discount compared to the $135 IPO price. They warn that investors are paying a steep premium for unproven AI narratives and distant Mars ambitions.

Massive Capital Consumption: Between Starship development, expanding the satellite constellation from 9,600 to an intended 100,000 birds, and building out massive AI data centers, SpaceX’s cash burn rate is unlike anything Wall Street has ever seen.

Frequently Asked Questions (FAQs)

What was the final SpaceX IPO valuation when it listed?

The official SpaceX IPO valuation was finalized at $1.77 trillion at its listing price of $135 per share on June 11, 2026. However, during its trading debut on June 12, strong market demand pushed the stock price up to $150, driving the company's real-time market cap past the $2 trillion mark.

Why is SpaceX losing money if Starlink is profitable?

While Starlink generated a highly impressive $4.4 billion in operating income in 2025, its profits are entirely offset by heavy capital expenditures in other divisions. SpaceX is pouring billions into Starship development and spending roughly $2.5 billion per quarter on high-end AI compute infrastructure following its merger with xAI.

How many subscribers does Starlink currently have?

As of June 2026, Starlink has surpassed 12 million active subscribers worldwide across its residential, commercial, maritime, and government service tiers.

Is Elon Musk the world’s first trillionaire?

Yes. Thanks to the strong market performance of the SpaceX IPO and his 42% equity stake (coupled with 85% voting control) in the newly public company, Elon Musk's net worth has officially crossed the $1 trillion threshold.

The Verdict: A High-Stakes Leap into the Future

The SpaceX IPO is not just another tech float; it is a profound historical marker. Investors buying shares of SPCX today are not buying a traditional aerospace business, nor are they buying a simple internet provider. They are funding a highly integrated ecosystem that combines global connectivity, orbital logistics, and cutting-edge artificial intelligence infrastructure.

The risks are undeniably massive. The ARPU erosion in international markets threatens Starlink's margins, the AI buildout is burning cash at an astonishing rate, and the timeline for Starship's commercial monetization remains highly uncertain.

However, for a company that has spent two decades turning "impossible" sci-fi concepts into highly profitable market realities, betting against Musk's ultimate space economy ecosystem could be an even bigger risk.

Stay Ahead of the Space Economy

Analyze the Markets: Track the live performance of SPCX and compare it against other tech giants on our Market Trends Dashboard.

Deep Dive into Tech Stocks: Read our comprehensive analysis on the Future of AI Infrastructure and xAI Integration.

Get Exclusive Insights: Sign up for our weekly newsletter to receive exclusive venture capital breakdowns and upcoming tech IPO alerts directly to your inbox.

Comments