Why Hedge Funds Sell Big Tech: The Strategic Shift Ahead of the Historic SpaceX IPO

- 1 day ago

- 6 min read

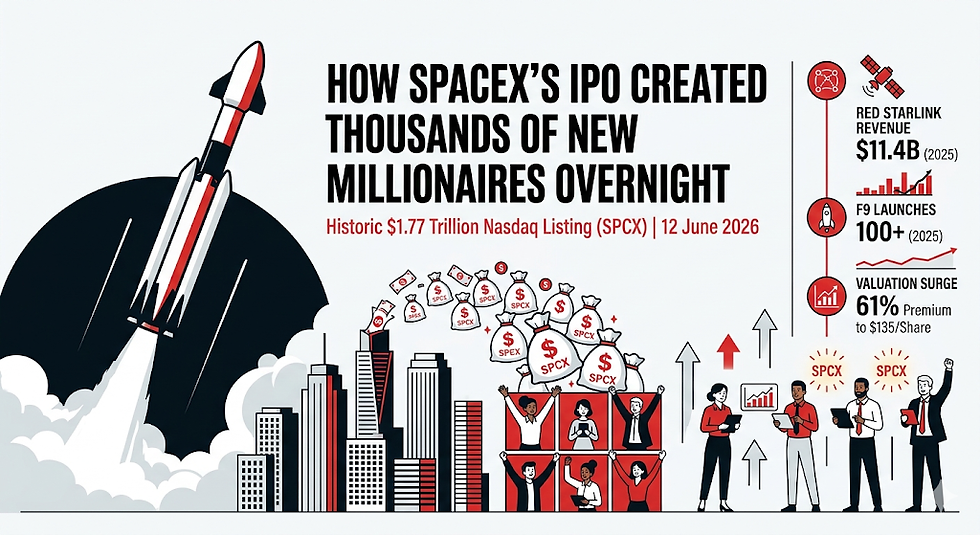

The financial landscape experienced a seismic disruption as Wall Street adjusted to the largest initial public offering (IPO) in financial history. On Friday, June 12, 2026, Elon Musk’s aerospace, satellite, and artificial intelligence giant, SpaceX, officially debuted on the Nasdaq under the ticker symbol SPCX.

Priced at a fixed $135 per share, the company raised a staggering $75 billion, elevating its market valuation to an eye-popping $1.77 trillion to $1.8 trillion. Upon the opening bell, shares instantly surged past $150, pushing SpaceX's market capitalization above $2 trillion and crowning Elon Musk as the world's first trillionaire.

Yet, the real story for institutional asset managers wasn't just what happened on the day of the launch, but the massive capital realignment that preceded it. In the days leading up to June 12, a major trend emerged across Wall Street: institutional investors began unloading their most reliable tech plays.

To capitalize on this historic market debut, institutional managers recognized that hedge funds sell big tech to unlock massive cash reserves, opting to lock in profits from standard AI gainers to clear room for a trillion-dollar aerospace monopoly.

This deep-dive investigation explores the underlying mechanics of this historic rotation, the specific data trailing the "Magnificent Seven" selloff, and what this structural realignment means for tech valuations throughout the rest of 2026.

The Tectonic Liquidity Shift: Unpacking the Numbers

According to data compiled from an internal JPMorgan institutional note, hedge funds aggressively trimmed their long positions in mega-cap U.S. technology firms. They even established tactical short positions in the broader software sector just days before the SpaceX launch.

The immediate casualty of this capital re-routing was the iconic "Magnificent Seven"—Nvidia (NVDA), Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Tesla (TSLA), and Microsoft (MSFT).

The table below outlines the market realities observed during the first two weeks of June 2026:

Impact of SpaceX IPO Prep on Major Tech Indicators

Metric / Financial Asset | Market Movement (June 5 – June 12, 2026) | Primary Driver |

Roundhill Magnificent Seven ETF | Declined by over 2.4% | Heavy institutional profit-taking and distribution. |

U.S. Software Industry Holdings | Deeply net-sold; substantial outflow | Rotation away from traditional software-as-a-service (SaaS) multiples. |

Semiconductor Sector (e.g., Nvidia) | Remained stable / Experienced "strong demand" | Unwavering systemic appetite for physical AI hardware components. |

Financial Sector ETFs | Strongly purchased; net inflow | Seasonal rotation paired with hedges in capital-intensive financial assets. |

SpaceX IPO Book Order Total | Over $250 Billion (3x to 4x oversubscribed) | Extreme demand from sovereign wealth funds, institutions, and retail clients. |

The scale of this migration becomes clearer when analyzing the macro landscape. Alphabet sought to raise nearly $85 billion via corporate equity maneuvers, while Meta contemplated a massive multi-billion-dollar share sale. Simultaneously, institutional players faced strict allocation cuts.

Because Elon Musk explicitly structured the allocation to favor retail investors—giving everyday traders an unprecedented 20% to 30% of the public float—and reserved heavy portions for long-only asset managers and sovereign wealth funds (such as Saudi Arabia’s Public Investment Fund, Qatar, and Kuwait), hedge funds found themselves severely squeezed. To secure a place in the remaining institutional book, they had to prove they had immediate, liquid "dry powder."

Why Hedge Funds Sell Big Tech to Fund Strategic Rotations

Institutional portfolio allocation is bound by rigid structural constraints. When a trillion-dollar monster like SpaceX lists on the public market, multi-strategy funds cannot simply buy in using margin or credit; they must alter their existing portfolios.

Understanding why hedge funds sell big tech comes down to three structural market catalysts:

1. Freeing Up Cash for an Overallocated, Oversubscribed Book

With total orders across the globe crossing $250 billion, the SpaceX IPO was heavily oversubscribed. Heavyweights like BlackRock placed initial bids exceeding $5 billion.

Because investment banks like Goldman Sachs, JPMorgan Chase, and Morgan Stanley aggressively sliced institutional orders to fulfill retail demand, hedge funds had to free up excess capital to ensure their downscaled allocations were funded with zero transactional friction. Selling top-tier liquid tech holdings like Apple and Microsoft near all-time highs was the fastest way to generate multi-billion-dollar cash positions.

2. The Great AI Evolution: From Earthbound SaaS to Orbital Infrastructure

Many macro analysts point out that institutional investors are experiencing a visible phase of fatigue regarding Earthbound artificial intelligence software plays. Traditional software multiples are trading at peak valuations, while SpaceX offered something entirely distinct: an unassailable orbital infrastructure play.

Beyond its foundational rocket launch dominance (completing more launches in recent years than entire sovereign nations combined), SpaceX recently integrated Musk’s xAI venture. The company's future value proposition relies heavily on building space-based AI data centers powered by its massive Starlink constellation and proprietary Colossus data installations.

Hedge funds realized that switching from an over-allocated software stock to a infrastructure-backed orbital AI business offered a far better risk-adjusted return profile for late 2026.

3. Fast-Track Index Inclusion Rules

Historically, massive IPOs were forced to undergo a lengthy "seasoning period," keeping them out of major benchmark indices for months or even a year. SpaceX shattered those historic guidelines.

Effective May 2026, both the Nasdaq-100 and FTSE Russell instituted accelerated "fast entry" provisions. The Nasdaq-100 adjusted its policies to allow companies with a market cap exceeding $100 billion to gain benchmark entry within just 15 trading days. FTSE Russell went a step further, implementing a rapid 5-day inclusion cycle for the Russell 1000 and 3000.

Hedge funds knew that passive index-tracking mutual funds and ETFs would be legally forced to acquire billions of dollars of SPCX stock almost immediately after launch. Buying early meant front-running that guaranteed passive structural demand.

The Broader Market Consequences: What Follows Next?

The capital shockwave sparked by the SpaceX debut will resonate through the financial sector for the rest of the year. Retail platforms like Fidelity lowered participation minimums to $2,000 to capture the massive surge in retail interest. Meanwhile, the broader tech indexes have faced an adjustment period as valuations equalize.

Crucially, this is not a short-term trend. The capital extraction we are seeing is part of a multi-stage primary market cycle.

With generative AI pioneers like Anthropic and OpenAI heavily tipped to execute their own highly anticipated public market listings later this year, institutional portfolios will need to remain uniquely liquid. The tactical playbook established to handle SpaceX's arrival will serve as the financial baseline for how institutional syndicates handle mega-cap tech arrivals moving forward.

Frequently Asked Questions (FAQ)

Q1: Why did hedge funds sell big tech right before the SpaceX public debut?

A: The primary reason hedge funds sell big tech ahead of large offerings is to create immediate liquidity. Because the SpaceX book was up to four times oversubscribed and drew over $250 billion in total orders, institutions needed to clear space on their balance sheets, lock in profits from fully valued tech companies, and accumulate cash to guarantee they could fulfill their allocations for the $75 billion listing.

Q2: What was the official offering price and valuation for the SpaceX IPO?

A: SpaceX utilized an unconventional, fixed-price book-building structure, skipping the traditional variable price range entirely. Shares were offered directly to the public at $135 per share. This fixed entry point established a base market capitalization of $1.77 trillion to $1.8 trillion, which quickly climbed past $2 trillion once active secondary trading began on the Nasdaq exchange.

Q3: How did the "Magnificent Seven" stocks perform during the IPO week?

A: The broader mega-cap tech sector experienced clear downward pressure. Tracking vehicles like the Roundhill Magnificent Seven ETF dropped by more than 2.4% in the week leading up to the June 12 listing. The selloff was particularly pronounced within major enterprise software holdings, while semiconductor and component hardware manufacturers maintained stable institutional demand.

Q4: What are the fast-track index inclusion rules affecting SpaceX?

A: To adapt to mega-cap private companies going public, major index managers updated their structural rules in May 2026. The Nasdaq-100 introduced a fast-track rule allowing companies valued over $100 billion to join the index within 15 trading days instead of waiting a year. FTSE Russell introduced an accelerated 5-day rule for the Russell 1000, ensuring passive index funds must buy the asset almost immediately.

Industry Research & Links for Further Analysis

Track Real-Time Market Data: To evaluate how global institutional funds are continuing to adjust their portfolios post-IPO, view the Nasdaq Market Activity Tracker.

Analyze Macro Technical Trends: To track historical fund flows out of mega-cap tech relative to primary offerings, explore JPMorgan Institutional Global Research.

Review Venture Capital and Secondary Private Holdings: To study how early-stage private valuations translate to current public listings, read the ClearTax Investment Analysis on Global IPOs.

Comments